Are we there yet?

On Foord International Fund’s 20th anniversary three years ago, portfolio manager BRIAN ARCESE analysed the fund’s performance across full market cycles. At the time of writing the prevailing market cycle was eight years long — incomplete but in its ninth innings. Where are we now?

The Foord International Fund aims to achieve meaningful, inflation-beating US dollar returns over rolling five-year periods with limited investment risk. It has a flexible but conservative investment policy. In the race between the tortoise and the hare it is without doubt the tortoise. Never fast out of the blocks, it wins in the spirit of ‘to finish first, first you must finish’.

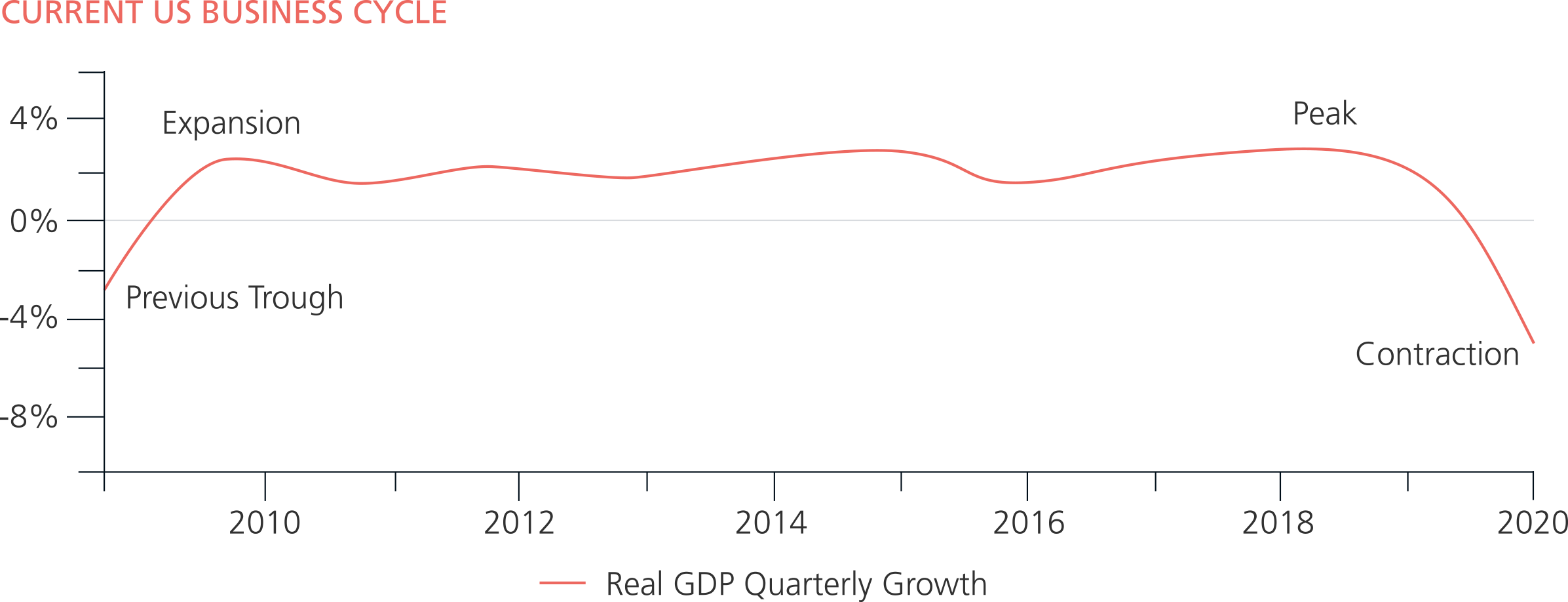

The business or economic cycle typically lasts six years and has four broad phases: expansion, peak, contraction and trough. My piece three years ago showed that the Foord International Fund typically lags during the expansionary and peak phases, but outperforms during the contractionary and trough phases to cross the cycle’s finish line first.

The US business cycle expanded for a record 11 years until it hit the COVID-19 speedbump in February 2020. Opinion is divided on whether the pandemic constitutes a black swan event (see Did You Know?). Its impact was undoubtedly material and it caught the world by surprise. US markets recorded their fastest-ever bear market correction and global economies will contract heavily this year.

Foord International Fund performed admirably through the market correction (see Weathering the COVID-19 Market Rout ). But share markets have mostly recovered to pre-pandemic levels on massive monetary and fiscal stimulus and hopes for a coronavirus vaccine this year. What then, if anything, could finally end the current investment cycle?

There are quite a few headwinds that could cause a(nother) significant market drawdown. First, COVID-19 is not under control in several large, important economies, including the United States. Failure to successfully manage the pandemic would weigh on growth more than markets are now pricing into global equities.

Second, if the US presidential election was held today, the Democrats through Vice President Biden would probably record a clean sweep, winning the White House and the Senate. This would usher in higher corporate and individual income tax rates and taxes on capital gains and dividends. S&P 500 index earnings would decline by 12% to 20%, with valuations falling accordingly.

Finally, US sovereign and corporate indebtedness is nearing all-time highs. Up to one-fifth of US corporates could effectively be insolvent. While the US Federal Reserve can address short-term liquidity crises, it is much less suited to solving solvency issues. Even in the absence of large-scale corporate defaults, this debt overhang could subdue economic growth for years.

Given these risks, Foord International Fund remains cautiously positioned and balanced, with returns not reliant on any one market outcome. The managers still hold hedged equity positions to mitigate market losses if some or more of these risks eventuate. We are keeping the liquidity powder dry to exploit these and future dislocations.