Safe harbour when shocks strike

March was a brutal month for investors. Oil surged, bonds fell and share markets sank as the war on Iran turned into a full-blown energy shock. Against that backdrop, Managing Director PAUL CLUER writes that Foord’s conservatively positioned funds held up well, showing again that capital preservation matters most when markets come under stress.

Investors began March in a reasonably cheerful mood. Inflation seemed to be fading, interest rates looked more likely to fall than rise, and the rich world appeared to have put its worst economic worries behind it. By month-end, the mood had changed sharply.

The Israeli-American attack on Iran, and the effective closure of the Strait of Hormuz to oil traffic, produced a classic supply shock. Brent crude surged 63% in March. Equities and bonds fell globally. Europe was among the worst hit. South African assets and the rand tumbled. Even gold came under pressure as investors sold what they could to raise cash.

What unsettled markets was not only the jump in energy prices, but the absence of any quick fix. Oil traders were not responding to diplomatic rumour so much as to physical reality: damaged infrastructure, disrupted shipping, scarcer insurance and the slower work of restarting production, refining and transport. Strategic reserve releases bought time but did not create supply. As so often in markets, hope and logistics were telling different stories.

It was in that setting that Foord’s safety-first investment positioning mattered. The Foord funds had for some time avoided the frothiest parts of the market and had been constructed more defensively than many peers. That caution was not a prediction of war, but an acknowledgement that expensive assets, narrow leadership and complacent markets leave little room for external shocks. Diversification, judicious asset allocation, a preference for safer equities and bonds, some non-correlated investments and derivative hedging at the margin all helped to soften the blow.

The result was that the Foord funds performed near the top of their respective peer groups in March. Given the market rout, this meant our funds typically declined much less than benchmarks and peers. Protecting investors against loss is, after all, a hallmark of the Foord investment philosophy.

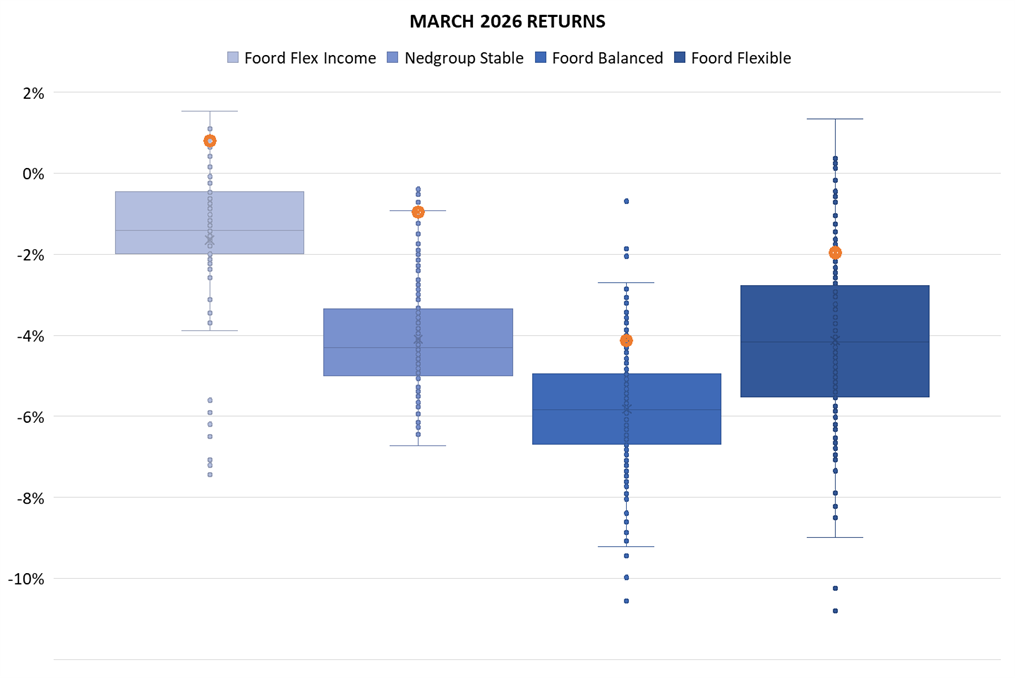

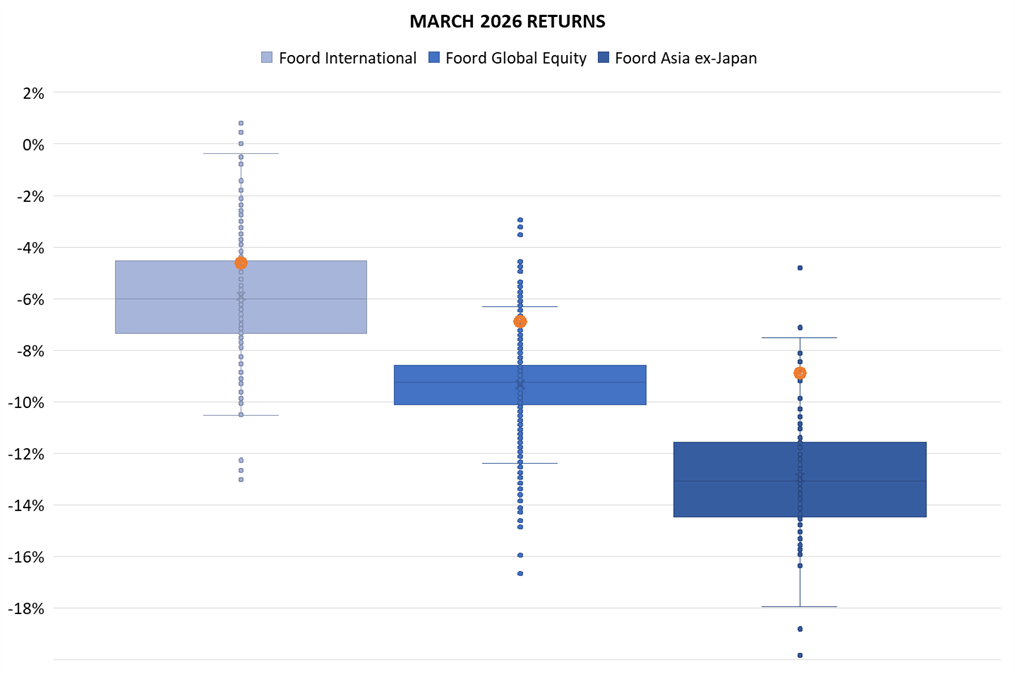

The box-and-whisker charts show the range of returns for the peer group sectors of Foord’s key investment strategies for March 2026. Each box contains the middle 50% of fund returns, while each whisker encloses the upper and lower quartiles. Outliers are shown as single dots, with the Foord funds shown as orange circles.

Every Foord fund shown outperformed at least 75% of comparable funds. Some ranked near the very top of their sectors for the month. Most encouragingly, the more defensive products did exactly what they were meant to do. The Foord Flex Income Fund and Nedgroup Investments Stable Fund stood out. In sectors designed for shorter time horizons and lower tolerance for loss, that resilience mattered. We were stunned that some peer group funds lost 6% or more in a single month.

Within the Foord global funds, the pattern was similar. Our Foord Asia ex-Japan Fund declined almost 9% but outperformed 90% of funds with a similar investment objective. A focus here on better quality companies at better valuations paid off. The same was true of the Foord Global Equity Fund. The Foord International Fund was perhaps not quite as resilient as might have been expected. The derivative hedges worked as designed, but the fund’s precious metals investments weighed on returns, with gold failing to offer protection in a month when liquidity mattered more.

March was an unusually vivid reminder that markets do not only rise and fall on earnings and interest rates alone. Politics can move inflation, currencies, capital flows and valuations all at once. In such conditions, portfolios built for several plausible outcomes, with liquidity preserved and balance maintained, are likely to prove more useful than those built around a single optimistic view of how quickly calm will return.